THE SCENARIO

Working with a note broker, I find a note that I can purchase. The terms of the note are as follows:

Borrower has stopped paying again.

THE QUESTION

A) If you approve the short sale at a net-to-you price of $65,000, and you get that money 5 months after their last payment, what would your total yield be?

B) If you approve a net-to-you price of $60,000 instead, what would your total yield be?

C) If you want 11% yield on your money, would you approve a net-to-you price higher or lower than $60,000?

THE SOLUTION

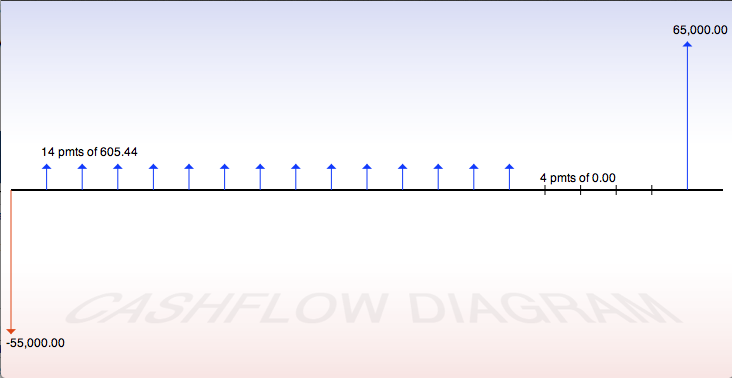

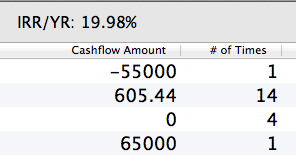

A) If you approve the short sale at a net-to-you price of $65,000, and you get that money 5 months after their last payment,what would your total yield be?

Uneven:

-$55,000 x 1

$605.40 x 14

$0 x 4

$65,000 x 1

IRR/YR = 19.98%

Your total yield would be 19.98% if you approved this short sale.

B) If you approve a net-to-you price of $60,000 instead,what would your total yield be?

Uneven:

-$55,000 x 1

$605.40 x 14

$0 x 4

$60,000 x 1

IRR/YR = 15.15%

Your yield would be 15.15%.

C) If you want 11% yield on your money, would you approve a net-to-you price higher or lower than $60,000?

You could accept less money.

-$55,000 x 1

$605.40 x 14

$0 x 4

??? x 1

Trial and error in using uneven cashflow analysis reveals that if you got $56,000, you would make 11.01% on your money. Whether or not you want to do this is up to you as the note holder.