Lastly, time for part 5. To recap, the scenario from Parts 1, 2, 3, and 4 is as follows:

THE SCENARIO

I came across a note for sale. The terms of the note are as follows:

Original balance: $6,000

Unpaid balance as of June 2: $4,560

Term: 5 years

Interest Rate: 0

Payments: $100 per month

If I buy it, make the purchase on June 2, and the first payment I'll receive will be the July payment.

Every February, the borrower pays off $1,000 in order to accelerate the note paydown.

QUESTION

The current owner of the note wants to sell me the note for15% off its face value (85% of $4,560 = $3,876).

If I want to get a 25% yield on the deal, and I expect the borrower to make his extra lum-sum payments every February, what's the most I can pay for the note?

SOLUTION

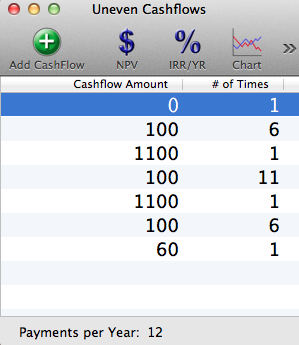

Because I want to find out what I'd pay, I zero out the Initial Cashflow on my Uneven Cashflow setup.

Graphically, that looks like this:

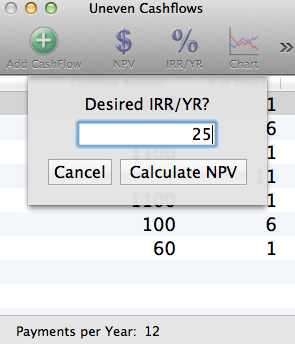

Then I hit NPV and enter my desired yield (25%).

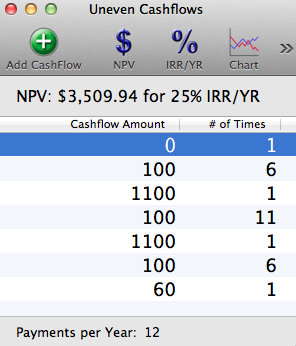

I discover that the most I can pay for the note is $3,509.94.

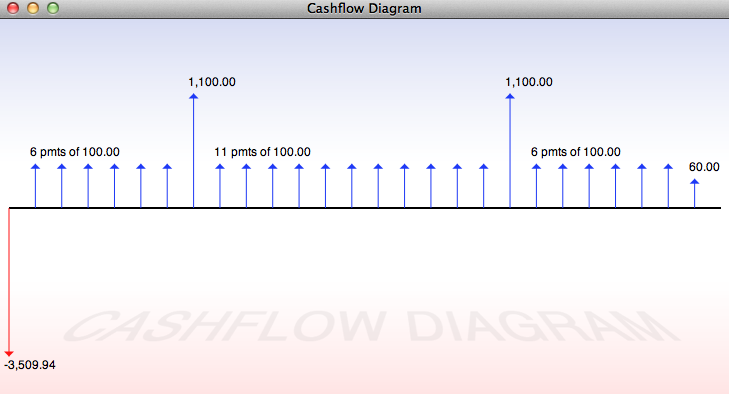

Here's the cashflow diagram for that:

All things considered, that doesn't seemthatfar off of the seller's asking price, so if I'm good at negotiating, I might be able to make that happen.

DISCUSSION

If you've gotten through all five parts, good job! Hopefully you've learned a thing or two that you can use in your own investing efforts.

Uneven Cashflow analysis lets us model some pretty complicated situations that more closely resemble the real world than straight TVM calculations can generally get us. Knowing how to do TVM is 100% essential for any investor, but knowing how to do more complicated analyses can really provide a competitive edge. It's definitely a good skill to have!

If you have any questions of your own, feel free to send them to us at theTeam@InADayDevelopment.com, and we just might turn them into a future Money Blog article! See you next time!